China Automotive Engine Market Survey Report

2021-04-30 07:02:48

Industry Development Overview

Most cars use reciprocating piston internal combustion engines that are fueled with gasoline or light diesel. The automobile is mainly used for transportation and requires a power device with small mass, light weight, fuel economy, good adaptability, and reliability and durability. The gasoline engine's power (power per cylinder displacement) is high, it is less than mass (mass per unit of power), it is easy to start, it has low vibration and noise, and it is used in most cars and light goods vehicles, some medium-sized passenger cars and trucks. Diesel engines have low fuel consumption and long overhaul mileage. They are used in heavy-duty vehicles and most medium-sized trucks as well as passenger cars. Due to the energy relationship, the use of diesel engines has continued to expand.

From 2000 to 2004, the proportion of the domestic automobile engine industry in GDP increased year by year, and its status in the national economy gradually increased. In 2005, the development of the automotive engine industry slowed down, and its position in the national economy also declined, but it was still higher than the ratio between 2000 and 2001. In 2006, it began to rebound.

From the data of the past seven years, the comprehensive economic benefits of the automotive engine industry have increased significantly, from very low 97.57 in 2000 to 228.31 in 2006, with a very large increase. The above data shows that the overall economic efficiency of the automotive engine industry is improving.

China automobile engine production and sales statistics analysis

Automotive starters are important automotive electrical products. In recent years, the Chinese auto market has grown at a rapid rate. In 2007, the sales volume of autos in China was 8.791 million. In 2010, the auto sales volume will reach 12.63 million. The automotive starter market also has huge business opportunities. In 2007, the production and sales volume of automotive starters in China's large-scale enterprises exceeded 16 million units, and the output and sales of generators exceeded 10 million units. The industry’s sales revenue exceeded 10 billion yuan and the profit was nearly 1 billion yuan. At present, there are more than 600 manufacturers of automobile starters and generators and their main parts and components in China, of which about 300 have overall machine production capacity. With the intensification of competition, the market segmentation in the industry has become increasingly clear. Domestic domestic starter and generators have a domestic matching market coverage rate of more than 99%, including domestic passenger cars, mini-vehicles, light vehicles, passenger cars, and trucks. Engineering and agricultural machinery, ships, etc. Among them, wholly foreign-owned and foreign-funded joint venture companies have rapidly expanded their markets and gradually become the main suppliers of matching machines for the passenger and commercial vehicle industries in China. The relatively fixed market competition pattern has enabled the industry to basically release its original production capacity. It can be predicted that a new round of large-scale investment in the industry will rise soon. From 2000 to 2006, the production and sales rate of the automotive engine industry was above the industry standard value of 96%, indicating that the industry's production and sales ratio was reasonable.

Table 1 Production and sales of automobile engines in 2005 and 2006

Third, the operating characteristics of the industry

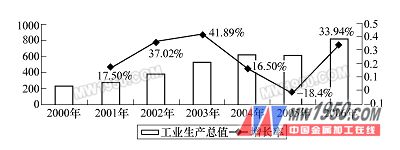

In 2006, the overall operating condition of the engine industry was relatively stable. As of the end of December 2006, according to the statistics from the National Bureau of Statistics, enterprises above designated size in the automotive engine industry have realized a total value of 73.701 billion yuan, up 15.13% year-on-year; industrial output value has reached 806.4153 trillion yuan, a year-on-year increase of 33.94%; and the main business income has been realized. 75,692,722 million yuan, an increase of 29.13% over the same period last year. From the industry indicator data, we can see that compared to 2005, the development of the automobile engine industry is in a better development trend, the scale of the company is relatively stable, the fixed asset investment of the whole industry is relatively increased, the scale of production is controlled, and the production efficiency is Increased. From 2000 to 2006, the market size and growth rate of the automotive engine industry are shown in Figure 4.

From 2000 to 2004, the total industrial output value of the automotive engine industry increased year by year. Among them, the fastest growth rate in 2003, the growth rate reached 41.89%; 2005 industrial output value fell by 1.84 percentage points to 60.2 billion yuan, an increase of 1.62 times compared to 2000; 2006 (33.94% growth rate) The total industrial output value reached 80.6 billion yuan, an increase of 57.6 billion yuan from 2000.

Analysis of Development Trend of Chinese Vehicle Engines

1. Development trend of gasoline engine

The gasoline engine market space is mainly affected by the development of the passenger car market. It is estimated that by 2010, the domestic car market will reach 5 million, and mini-buses will remain around 900,000. Therefore, there is huge room for growth in the gasoline engine market.

Table 2 Demand Forecast of Cars and Microbuses Market 2008-2010

In the future, the demand for large and medium-sized diesel engines will further develop in the direction of “lower displacement, higher compression ratio, and higher powerâ€.

At present, the domestic large-scale diesel engine can achieve a power increase of 25kW/L, and it will develop to 30kW/L in the next 3-5 years. The mid-engine lifting power will also have a certain increase.

In the mid-term (5 to 10 years), the total mass of 25 t or more will develop to about 10 kW/t, and the t-power of heavy-duty vehicles will reach 8.5 to 9 kW/t in the past five years. The demand for engine power of heavy-duty vehicles with a capacity of over 25 tons in the next 10 years is mainly concentrated between 280 and 440 kW.

In the next 5 to 10 years, the total market demand for medium-sized engines will fluctuate within a certain range and there will be no excessive increase or decrease.

3. Development trend of light diesel engines

With the needs of economic development in urban and rural areas, the substitution of light trucks for agricultural vehicles has become one of the features of the future demand growth of the light-duty diesel engine market. The total demand for light-duty diesel engines in the market will show a rapid upward trend.

The implementation of higher emission regulations and fuel consumption regulations in China will promote the growth of the market share of medium and high-grade light diesel engines.

The degree of dieselization of light trucks is already very high. In the future, the dieselization of light passenger vehicles, SUVs, and pickup trucks will become one of the important growth points for the expansion of the light-duty diesel engine market.

The dieselization process of sedans will hardly be greatly developed in the next five years.

As policies encourage environmental protection and energy conservation, large-displacement passenger vehicles will be subject to certain restrictions; and as the level of technology increases, excessive displacement will also be a waste for the vehicle itself. In the future, the diesel engine for passenger cars will be mainly focused on 2.0L or less; the displacement range for commercial light vehicle diesel engines will be mainly concentrated in 2.0-3.5L.

EJ Industrial Group Co.,Ltd is a leading professional valves manufacturer in China.

our main products line are for water system service which include cast iron and ductile iron gate, globe, check, eccentric plug, and butterfly valves. We provide both types of metal to metal seat and resilient seat.

Swing Check Valve,Resilient Seated Valve,Resilient Seated Check Valve,Resilient Check Valve

EJ Industry Professional Valve Manufacture , https://www.ej-industry.com